News and Insights

.webp)

Scarcity and Compounding: Building Wealth In a Leveraged World

The Moment I Passed on Bitcoin

I remember the exact moment a friend told me to put money into bitcoin. He said there would only ever be 21 million coins. At the time, it was trading for just a few hundred dollars. The pitch was straightforward: digital scarcity, technological disruption, and an asset that could not be printed at will like government currencies.

I passed. I did not fully understand the appeal at the time, and more importantly, I did not view it as an investment in the same way I viewed owning productive businesses. Stocks represented ownership in companies that generated earnings, reinvested capital, and created value. Bitcoin felt speculative, and in some ways, it still does.

More than a decade later, I still prefer owning high-quality businesses. But the broader conversation has evolved. This is no longer just about bitcoin. It is about inflation, government debt, currency durability, and how investors think about preserving purchasing power in a financial system increasingly shaped by leverage.

That is where gold, silver, and bitcoin begin to intersect.

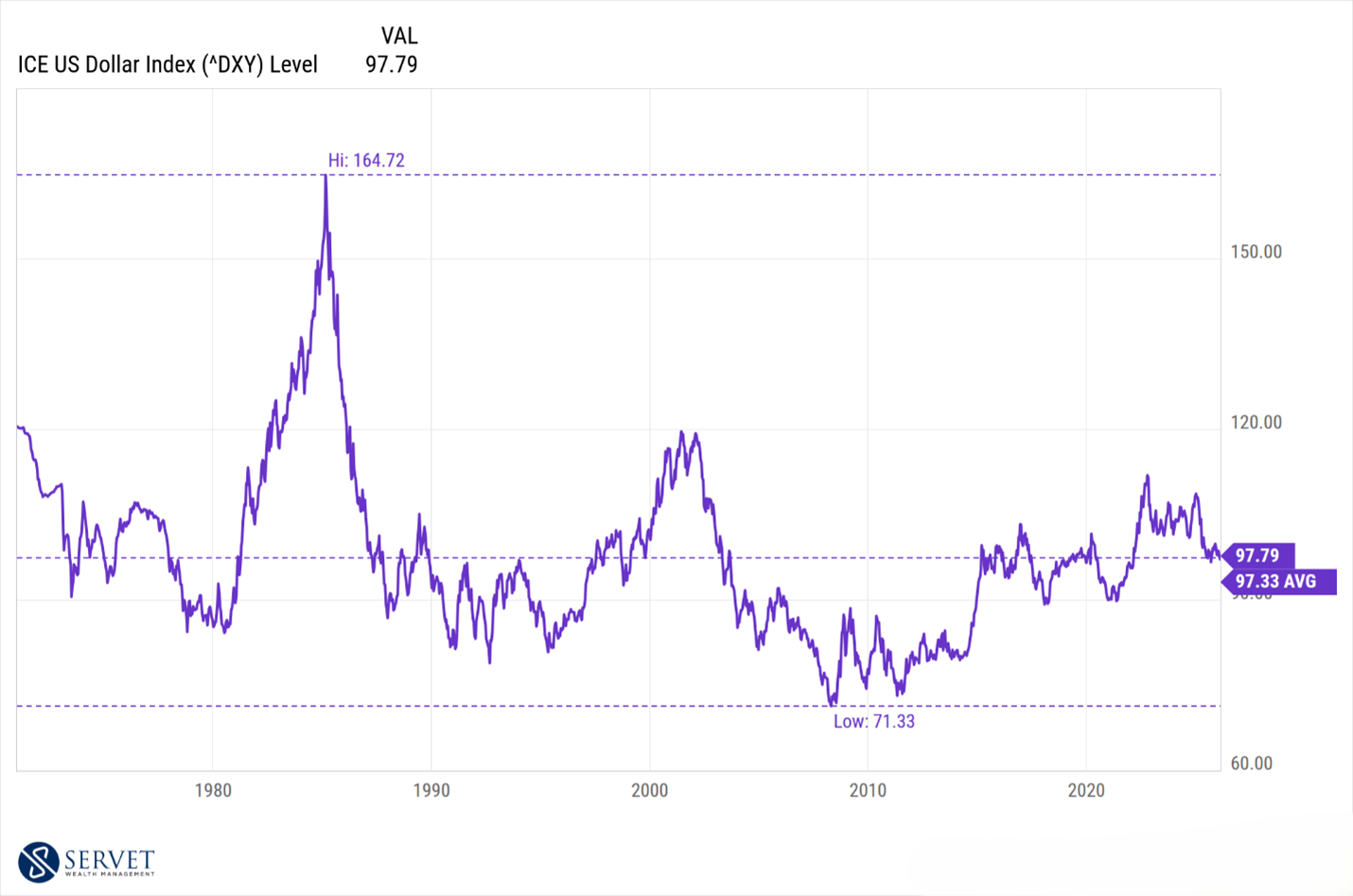

The Dollar in Transition

The U.S. dollar currently sits near long-term averages, even after reaching multi-year highs in recent years. Over the past year, its trend has softened as expectations for slower inflation and eventual rate cuts have taken hold. Currency markets are highly sensitive to interest rate differentials, and when investors anticipate lower relative yields, the dollar can lose momentum like we’ve seen the past year.

In recent months, the dollar has softened as expectations around slower inflation and potential rate cuts have taken hold. Currency markets are highly sensitive to changes in relative interest rates, and when investors anticipate lower yields in the United States, the dollar can come under cyclical pressure.

Historically, however, the dollar has tended to strengthen when the U.S. economy is growing faster than its peers and when interest rates are higher relative to other developed nations. Global capital generally moves toward stability and yield. During periods of geopolitical stress or financial uncertainty, investors often seek the liquidity and depth of dollar-based assets, reinforcing its role as the world’s reserve currency.

At the same time, longer-term structural questions remain in the background. The United States continues to run sizable fiscal deficits, and total government debt has risen meaningfully over the past two decades. According to data from the Federal Reserve Bank of St. Louis, the debt-to-GDP ratio now sits near 121 percent as of the third quarter of 2025. When debt grows faster than the underlying economy for extended periods, it does not necessarily create an immediate crisis, but it can gradually influence expectations about long-term purchasing power.

Both forces can operate simultaneously. The dollar may experience cyclical weakness or strength depending on interest rate dynamics, while investors continue to evaluate the longer-term fiscal trajectory. Understanding that distinction is important. Gold, silver, and bitcoin are often framed as alternatives to traditional currency exposure, but investors do not need to believe the dollar is collapsing to consider diversification. It is enough to recognize that fiscal policy, interest rate cycles, and debt trends shape currency outcomes over time.

Gold: Insurance Against Monetary Instability

Investors typically own gold for a few core reasons. First, it has historically served as a store of value during periods of inflation, currency weakness, and monetary instability. Unlike bonds or cash, gold is not tied to the promise of a government or corporation. It also has a role in jewelry and cultural traditions that date back thousands of years.

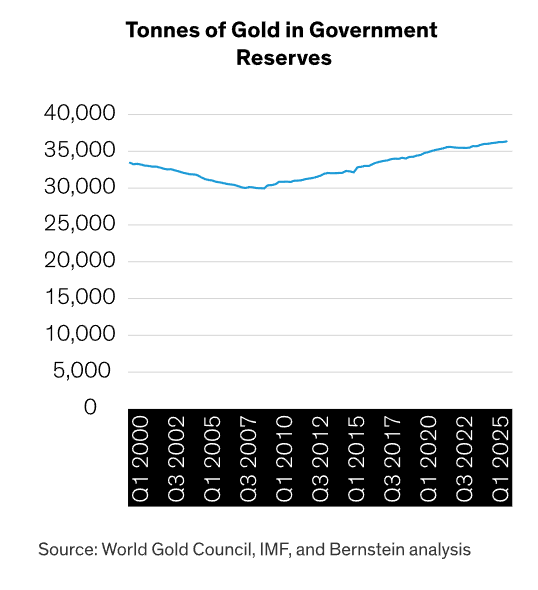

That characteristic becomes more appealing when government debt levels are rising or when investors begin questioning long-term fiscal discipline. In recent years, gold has also benefited from increased central bank buying as countries diversify their reserves beyond a single currency. When sovereign entities adjust reserve allocations, that demand is often structural rather than speculative.

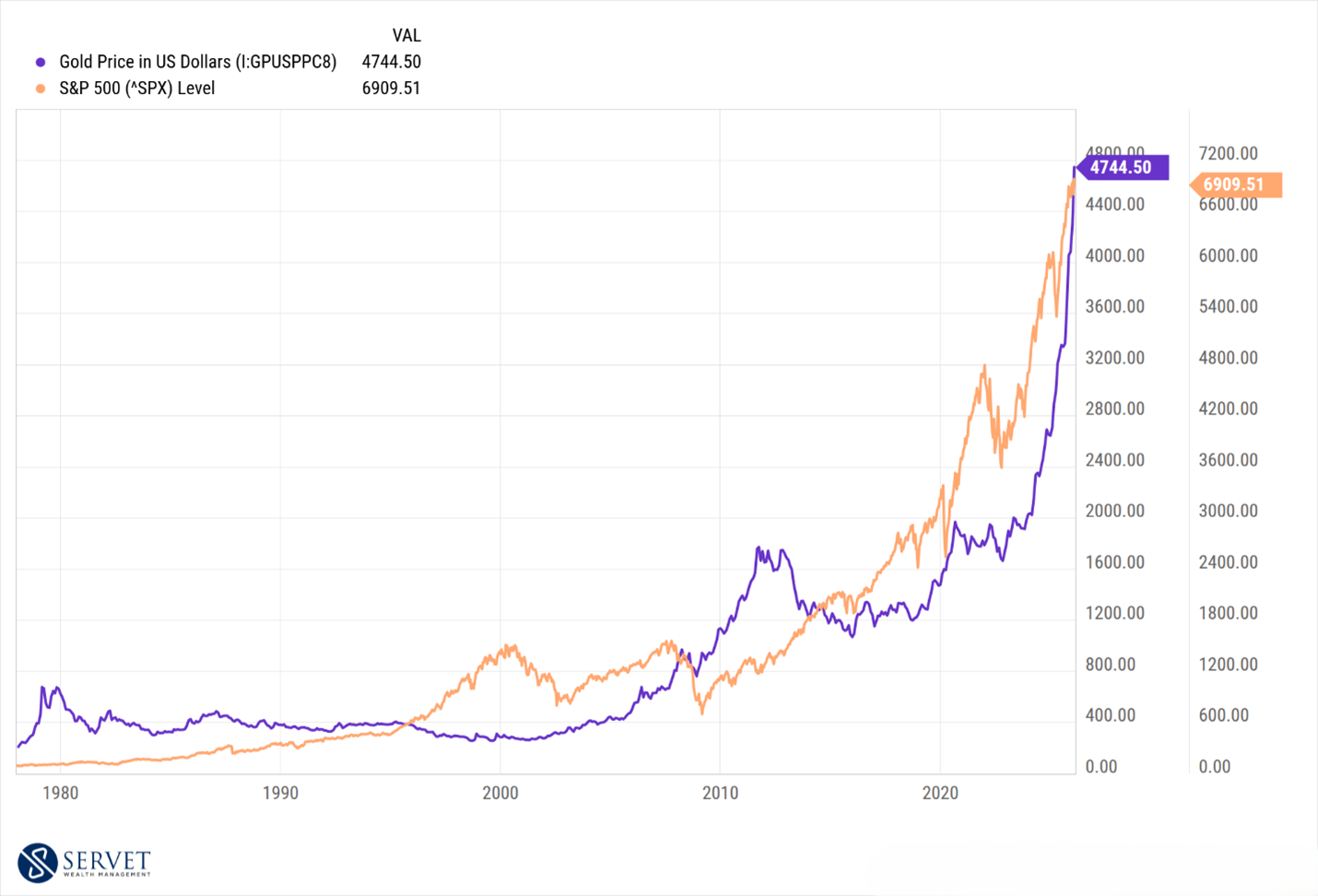

That said, owning gold is not a guaranteed hedge against every period of rising debt or fiscal expansion. There have been long stretches where government debt increased and deficits expanded, yet gold delivered muted or even negative real returns. After peaking around 1980, gold declined sharply and then spent nearly two decades underperforming, even as U.S. debt levels continued to grow and real interest rates declined.

So that leaves the question: is the recent move driven primarily by renewed concern around fiscal sustainability, or are we witnessing a more gradual structural shift as central banks continue to add gold to their balance sheets? It may be a combination of both. Over time, what tends to matter more are real interest rates, inflation expectations, and currency strength. Gold often performs best when real yields are falling, when inflation surprises to the upside, or when confidence in fiat currencies weakens. Outside of those environments, it can remain flat for extended periods.

That balance is important when considering how much gold belongs in a long-term portfolio. It can play a valuable role in diversification, particularly during periods of monetary stress.

Silver: Silver and the Risk of Speculation

Silver occupies an unusual position. It shares some of gold’s monetary characteristics, but it also has significant industrial applications in electronics, solar panels, and manufacturing. That dual identity can make its price behavior more volatile. When monetary demand rises, silver can move quickly. When industrial demand weakens, it can retrace just as sharply.

History provides a clear example of how silver’s volatility can accelerate under speculative conditions. In the late 1970s, the Hunt brothers accumulated massive physical holdings of silver and used significant leverage through futures contracts in an attempt to control supply and drive prices higher. Some estimated that they acquired over 1/3 of the world’s supply.

In early 1979, silver traded around $6 per ounce. By January 1980, it had surged to nearly $50 per ounce, an increase of more than 700 percent in less than a year. The move was fueled not only by inflation fears, but also by concentrated buying and aggressive leverage.

Then the rules changed.

Commodity exchanges increased margin requirements and limited the ability to open new long positions. As leverage was forced out of the system, silver collapsed. Within months, prices fell below $11 per ounce, and over the following years drifted back toward the low teens. The Hunt brothers ultimately faced massive losses and bankruptcy.

That episode does not mean today’s environment is identical. But it illustrates how quickly silver can detach from fundamentals when leverage and momentum dominate the narrative.

It also raises an important question for investors: why own silver? If the answer is simply that the price has been rising, that is not a thesis. That is an outcome. Silver can serve a role in a diversified portfolio, particularly given its industrial and monetary characteristics. But history shows that when positioning becomes crowded and speculative, volatility can accelerate just as quickly on the way down.

Bitcoin: Digital Scarcity in a Liquidity-Driven World

Bitcoin begins with a simple idea. There will only ever be 21 million coins. It operates on a decentralized network, not through a central bank. It cannot be printed or expanded by policymakers. It is portable, divisible, and can be transferred globally.

At its core, the thesis is about digital scarcity. In a world where government debt continues to rise and central banks have expanded the money supply during crises, an asset with a fixed supply can be appealing.

In that sense, the reasons investors buy bitcoin often overlap with the reasons they buy gold. Both sit outside the traditional fiat system. Both are viewed by some as protection against currency debasement. Both tend to attract attention during periods of monetary expansion.

Where bitcoin differs is in how it behaves. Historically, it has been much more sensitive to liquidity. When financial conditions are easy and capital is abundant, bitcoin has tended to rise sharply. When liquidity tightens, it has also fallen sharply. That pattern makes it far more volatile than gold.

The growth of institutional participation has added another layer. One prominent example is Michael Saylor and his company, Strategy, which used debt and equity to accumulate large bitcoin holdings. During strong rallies, that approach produced extraordinary gains. But leverage works both ways. When bitcoin declines, concentrated exposure can magnify losses just as quickly. You see this as the rise and fall of his publicly traded stock.

That does not invalidate the scarcity argument. But it does reinforce an important distinction in how there can be significant leverage even within it’s own system.

As with gold and silver, the key question is not whether the asset can rise. The question is what role it should play, how large that role should be, and whether the investor understands the volatility that comes with it. I can appreciate both sides of the argument for owning or not owning bitcoin.

For those who choose to own it, the allocation should be sized appropriately, in a way that would not materially disrupt their long-term financial plan if it were to experience significant drawdowns or even fail to meet its long-term expectations.

Bringing it back to First Principals

Gold, silver, and bitcoin each have a thesis. Each has environments where it can perform well, and each can serve a purpose within a diversified portfolio. But I continue to come back to a simple idea: productive assets compound.

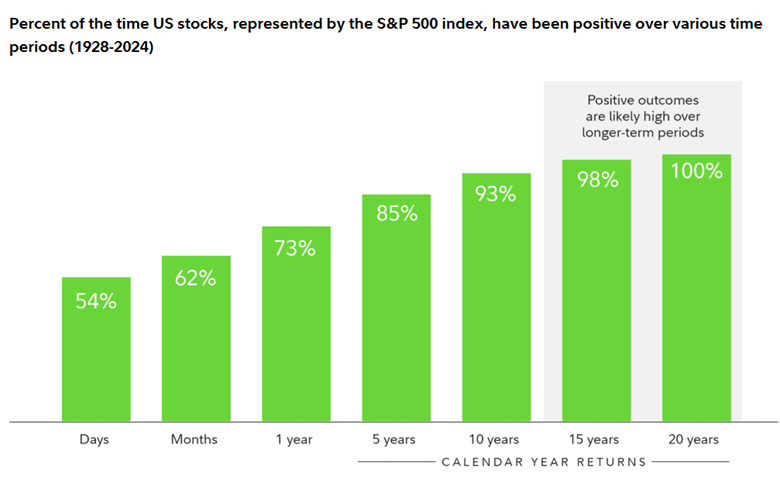

Owning high-quality businesses means owning companies that generate earnings, reinvest capital, and grow over time. That growth is not linear. Markets fluctuate, and volatility is part of the experience. Yet when the time horizon extends, the historical record becomes clearer. Data compiled by Fidelity shows that since 1928, U.S. stocks represented by the S&P 500 have been positive a little more than half the time on any given day. Over one-year periods, that probability rises meaningfully. Over five and ten years, it improves further. Over twenty-year periods, the historical outcome has been consistently positive.

Of course, past performance is never a guarantee of future results. History provides context, not certainty. The purpose of reviewing long-term data is not to promise outcomes, but to understand probabilities and align expectations with time horizons.

That does not mean alternative assets lack merit. Diversification has value, both across asset classes and within equities themselves. Different assets respond differently to inflation, liquidity cycles, and currency pressures. There may be room for gold, silver, or bitcoin within a portfolio, particularly for investors who understand the role each is meant to serve.

This is only the beginning of the conversation. The question is not whether one asset is superior to another, but how each fits within a disciplined allocation strategy. The more important exercise is asking what you need your capital to do over the next year, the next decade, and beyond, and then building a portfolio that reflects both that timeline and your comfort with volatility.

Let's Meet!

.webp)

About the author: Nathan Lee is a CERTIFIED FINANCIAL PLANNER® and Behavioral Financial Advisor at Servet Wealth Management in New York City. He works with individuals and families navigating important financial decisions, including retirement planning, tax strategy, investing, income planning, and wealth management. Through his blog and YouTube channel, Nathan explains complex financial topics in a practical, easy-to-understand way.

I read every email and would love to hear if this blog helped you.

.png)

.png)