.png)

%201.png)

News and Insights

The Magnificent 7 Are Lagging in 2026. Is AI Spending the Reason?

For the last few years, the Magnificent 7 helped carry the market. When investors talked about the S&P 500, they were often really talking about Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta, and Tesla.

But so far in 2026, that leadership has flipped.

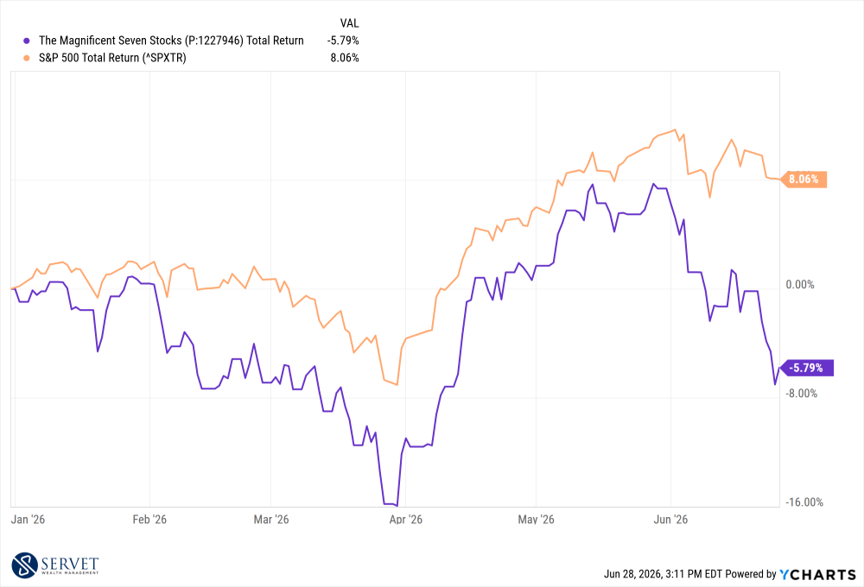

As of the YCharts data in the chart below, the Magnificent 7 basket is down 5.79% year-to-date, while the S&P 500 is up roughly 8%. Even more interesting, every individual Magnificent 7 stock shown in the chart is trailing the S&P 500 this year.

Chart 1: Magnificent 7 vs. S&P 500 YTD

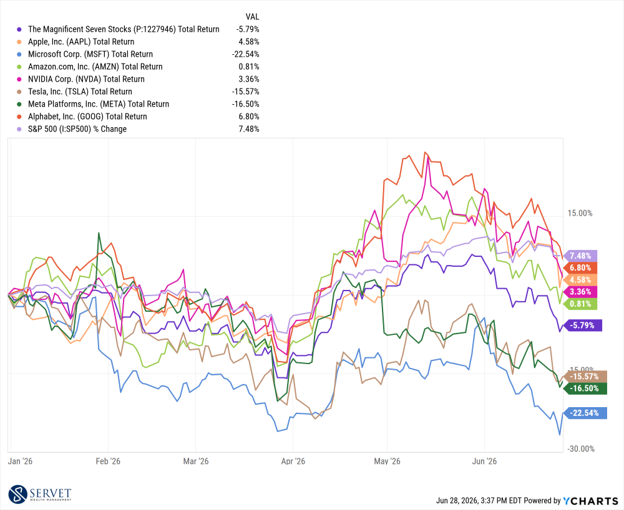

The second chart breaks this down further. While the S&P 500 is positive year-to-date, the individual names are mixed, but none are ahead of the index. Microsoft, Tesla, and Meta have been the bigger drags, while Apple, Alphabet, Nvidia, and Amazon have held up better but still lagged the broader market.

Chart 2: Individual Magnificent 7 Stocks vs. S&P 500

This raises a natural question: Why are some of the most profitable companies in the world suddenly lagging?

The answer is not that these companies have suddenly become bad businesses. Most of them are still highly profitable. The concern is that a growing share of their cash flow is being redirected into one massive bet: AI infrastructure.

The AI Race Is Turning Asset-Light Businesses Into Capital-Heavy Businesses

Historically, one of the reasons investors loved many of these companies was that they could grow without needing the same level of physical investment as traditional industrial businesses. Software, advertising, cloud, app stores, and digital platforms can be very profitable when they scale. They also benefited from high profit margins.

But AI has started to change that math.

Training and running AI models requires enormous amounts of computing power. That means more data centers, more servers, more networking equipment, more chips, more power, and more cooling capacity.

In other words, the market is starting to ask whether some of these businesses are becoming less “asset-light” than investors previously assumed.

Alphabet said in its March 2026 filing that capital expenditures rose from $17.2 billion in Q1 2025 to $35.7 billion in Q1 2026, and that it expects to significantly increase investment in technical infrastructure, including servers, network equipment, and data centers.

Amazon said it expects spending in technology and infrastructure to increase over time as it adds infrastructure and employees, including to support artificial intelligence and machine learning initiatives. Amazon also specifically warned that this spending can negatively impact short-term free cash flow.

Meta’s filings show the same pattern. Meta reported that construction in progress includes costs mostly related to data centers, network infrastructure, and servers. In its 2025 results, Meta also reported $72.22 billion of capital expenditures, including principal payments on finance leases, for the full year.

The market is not necessarily questioning whether these companies can make money. It is questioning how much cash they will need to spend before the AI payoff becomes clear.

And you can start to see it in this graph.

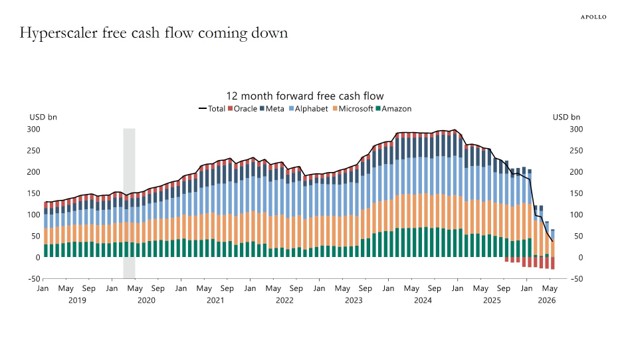

The third chart helps explain why investors are paying attention.

Chart 3: Hyperscaler Free Cash Flow Coming Down

While this isn’t directly the mag 7, it does represent the theme we are seeing. It shows 12-month forward free cash flow for major hyperscalers coming down sharply.

Earnings can still look strong while free cash flow weakens. A company can report positive net income, but if it is spending heavily on data centers, servers, and AI infrastructure, less cash may be left over for buybacks, dividends, debt reduction, or balance sheet flexibility.

That is the tradeoff investors are wrestling with right now.

On one hand, these companies may be building the infrastructure layer for the next major technology platform. On the other hand, they are committing hundreds of billions of dollars before anyone knows exactly how the economics of AI will settle.

Recent estimates suggest the largest hyperscalers — Microsoft, Alphabet, Amazon, and Meta — could spend hundreds of billions of dollars in 2026 alone on AI and related infrastructure. One estimate put the combined 2026 spending range at roughly $635 billion to $665 billion. Another report cited projections closer to $725 billion, up sharply from the prior year.

The exact number will vary by source and by what is included, but the direction is clear: AI is becoming a capital spending arms race.

The Main Risk: Spending Today for an Uncertain Payoff Tomorrow

This is the part investors are trying to price.

The AI buildout may prove to be one of the most important investment cycles in modern technology. These companies may be right to spend aggressively today because the future winners could control the infrastructure, models, distribution, and applications of AI.

But there is also risk.

The risk is that the spending comes first, while the revenue and profits arrive later than expected. Or that competition drives down returns. Or that everyone builds too much capacity at the same time. Or that the killer AI business model is not as profitable as hoped.

This is why the market can punish a company even when its earnings are still positive. Investors are not only looking at current profits. They are asking: How much future free cash flow will be left after this investment cycle?

But Doing Nothing May Be Risky Too

The other side of the argument is just as important.

For Microsoft, Amazon, Alphabet, Meta, and Nvidia, sitting out the AI infrastructure race may be even riskier than spending aggressively. If AI becomes the next dominant computing platform, the companies that underinvest could fall behind.

That makes this different from a normal capital spending cycle. This is not just about building more warehouses or office space. This is about protecting strategic position.

AI could affect search, cloud computing, advertising, software, e-commerce, chips, consumer devices, and enterprise productivity. These companies are not simply chasing growth. They may also be defending their existing businesses, or in some cases like Google, actively changing it.

How often do you click into a website when you Google something now? That push into AI answers is directly affecting their advertising model that made them so powerful to begin with.

So yes, this is a risky gamble.

But it may also be even riskier not to make it.

We Have Seen a Version of This Before With Meta

There is a recent example investors remember: Meta’s metaverse spending. It was so important to the company, they changed their name to reflect it!

In 2021 and 2022, Meta committed heavily to the metaverse through Reality Labs. Investors became concerned that the company was spending too aggressively on a long-term vision with an uncertain payoff. Reality Labs produced large losses, including a reported $13.7 billion operating loss in 2022.

Then Meta changed their minds.

The company shifted toward what Mark Zuckerberg called the “year of efficiency” in 2023, reduced costs, refocused investor attention on the core business, and free cash flow improved. The stock followed.

That does not mean today’s AI buildout will end the same way. AI infrastructure is more central to these companies’ core businesses than the metaverse was for Meta. But the market lesson is similar: when investors worry that spending is open-ended, the stock can struggle. When investors regain confidence that spending will produce returns, free cash flow can matter again.

The Big Question for the Next Year

The key question for the Magnificent 7 is no longer just, “Are these great companies?”

Most of them still are. The better question is:

Will the AI spending generate enough future cash flow to justify the capital being committed today?

That is what investors will be watching over the next year.

If revenue growth from AI, cloud, advertising, and enterprise adoption accelerates enough, today’s spending may look smart in hindsight. But if free cash flow keeps falling and the payoff remains unclear, the market may continue to treat these companies less like asset-light compounders and more like capital-intensive infrastructure businesses waiting for big profitability to return.

For long-term investors, this does not automatically mean the group should be avoided. The next phase will likely depend less on AI excitement and more on something much more important.

Can these companies turn massive AI spending into durable, profitable free cash flow?

Let's Meet!

About the author: Nathan Lee is a CERTIFIED FINANCIAL PLANNER® and Behavioral Financial Advisor at Servet Wealth Management in New York City. He works with individuals and families navigating important financial decisions, including retirement planning, tax strategy, investing, income planning, and wealth management. Through his blog and YouTube channel, Nathan explains complex financial topics in a practical, easy-to-understand way.

I read every email and would love to hear if this blog helped you.

.png)

.png)