News and Insights

.webp)

Understanding the Tradeoffs in Early Retirement

Healthcare, Taxes, and the Planning Window Many Retirees Overlook

Reaching age 60 with over $2 million saved for retirement places you in a position many people spend decades trying to reach. At that point, the question is often no longer whether retirement is possible, but whether continuing to work meaningfully improves your financial situation. For many households, the years between age 60 and Medicare eligibility at 65 create one of the most important planning windows in retirement. During this time, income often falls temporarily, creating opportunities to structure taxes, manage healthcare costs, and reposition retirement assets.

However, these years also introduce trade offs that are not always obvious. Early retirees must carefully navigate two key decisions: how healthcare costs will change once employer coverage ends, and whether to prioritize income strategies that qualify for ACA subsidies or use the opportunity to complete Roth conversions while tax brackets are relatively low. Understanding how these trade offs interact can significantly influence the long-term efficiency of a retirement plan.

The Risk Many High Savers Don’t Expect

When people think about retirement risk, they often focus on market volatility, inflation, or the possibility of running out of money later in life. While those risks certainly matter, in practice I often see something else become the primary challenge. Many individuals who have accumulated significant wealth continue working longer than necessary because the goalposts keep moving. Someone who reaches $2 million begins thinking about $3 million. Someone with $3 million starts aiming for $5 million. Eventually the conversation shifts from whether retirement is financially feasible to whether it feels psychologically comfortable.

The issue is that retirement planning cannot remain purely about accumulation forever. At some point the focus must shift toward using the wealth that has already been created. For many people, reaching their early sixties represents the stage where that transition begins.

Why Healthcare Becomes One of the Largest Early Retirement Expenses

Healthcare is consistently ranked as one of the largest financial concerns for households approaching retirement.

While working, most individuals receive health insurance through their employer, and that coverage is typically subsidized. Employers often pay a significant portion of the monthly premium, which keeps costs manageable for employees. Once someone retires before Medicare eligib ility at age 65, that employer subsidy disappears. Some retirees temporarily extend coverage through COBRA, but many eventually transition to purchasing private insurance through the Affordable Care Act marketplace. Over the past several years, enhanced premium tax credits dramatically reduced the cost of those marketplace plans, allowing millions of Americans to obtain coverage at significantly reduced monthly premiums.

As subsidies expanded, enrollment in ACA marketplace plans increased substantially. However, changes beginning in 2026 returned the system closer to its original structure, meaning that some households may no longer qualify for the same level of financial assistance.

Understanding the Federal Poverty Level and ACA Subsidies

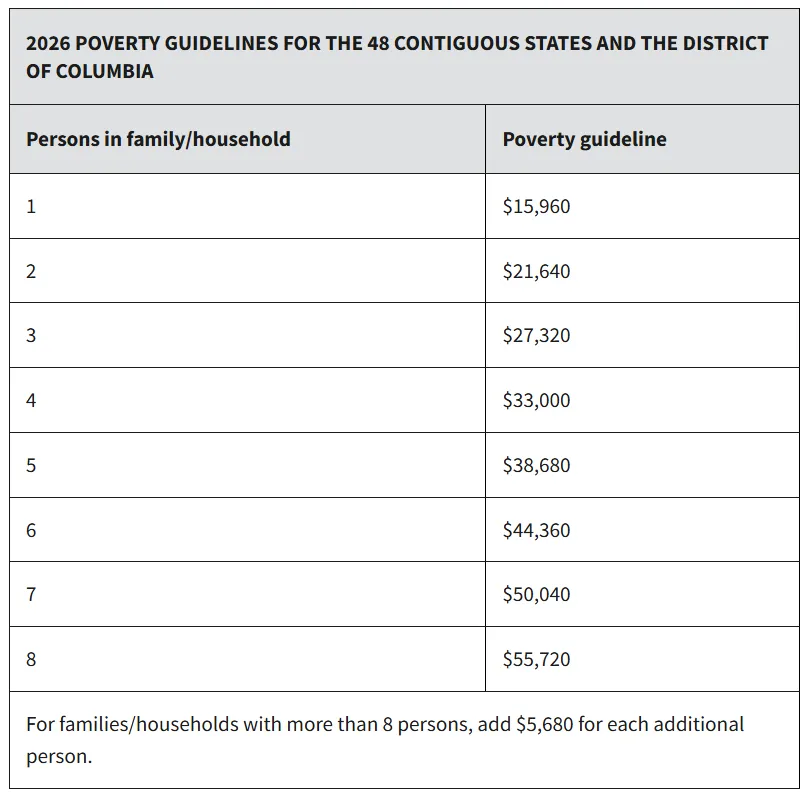

Eligibility for ACA subsidies is based on the Federal Poverty Level, commonly referred to as FPL.

The federal poverty level is an income benchmark used by the government to determine eligibility for various programs. The number changes depending on household size. For example, in 2026 the poverty guideline is $15,960 for a single individual and $21,640 for a household of two. Rather than using the poverty level itself, the ACA measures income as a percentage of that number. This is why you often hear references to income levels such as 150%, 300%, or 400% of the federal poverty level.

Under the standard ACA rules that returned in 2026, subsidies generally apply to households earning up to about 400% of the federal poverty level. Once income rises above that threshold, subsidies may disappear entirely.

This creates what analysts often refer to as the ACA subsidy cliff.

The subsidy cliff occurs when a relatively small increase in reported income results in a sudden loss of healthcare subsidies. When subsidies are available, premiums tend to remain relatively stable as a percentage of income. However, once income crosses certain thresholds, healthcare costs can increase sharply.

For example, the cutoff for a single individual in 2025 was $62,600 in many scenarios. Once income exceeds that level, the percentage of income spent on healthcare can jump dramatically. In some cases, healthcare costs may represent more than 20 percent of income for individuals in their early sixties purchasing coverage on the marketplace.

To understand the impact of losing subsidies, consider an example of a 60-year-old purchasing a plan through the ACA marketplace. With subsidies in place, a silver plan may cost roughly $449 per month. Without subsidies, that same plan could cost approximately $1,326 per month.

For a married couple retiring early, those costs could roughly double. This means healthcare alone could exceed $30,000 per year before Medicare begins.

Because of this, income planning becomes just as important as budgeting when evaluating early retirement.

Why MAGI Matters More Than Spending

Many retirees begin planning by estimating how much they expect to spend each year. For example, someone might determine that they need $80,000 annually to support their lifestyle. However, when it comes to ACA subsidies, the more important number is not spending but Modified Adjusted Gross Income (MAGI).

MAGI includes a variety of income sources commonly used in retirement. Withdrawals from traditional IRAs or 401(k)s count as income. Roth conversions count as income as well. Capital gains from selling investments may also increase MAGI, even if they are taxed at relatively low rates. Without careful planning, these sources of income can unintentionally push retirees above subsidy thresholds.

The Tax Valley Opportunity

When projecting taxes across an entire retirement timeline, income often follows a pattern that resembles a valley. Taxes are typically highest during working years, when wages and salary income are at their peak. After retirement, income may temporarily drop. Later in retirement, taxes can rise again once Social Security benefits begin and required minimum distributions start from retirement accounts.

The period between retirement and these later income sources is often referred to as the tax valley. During this window, many retirees find themselves temporarily in lower tax brackets.

Using Roth Conversions During Early Retirement

The tax valley creates an opportunity for Roth conversion strategies. During these years, retirees may convert portions of their traditional IRA into a Roth IRA while remaining in relatively low tax brackets. Instead of waiting for Social Security and required minimum distributions to increase taxable income later in retirement, retirees gradually convert portions of their retirement accounts while taxes are lower.

Over time, this strategy can reduce the size of traditional retirement accounts, lower required minimum distributions, and create tax-free income sources later in retirement. It may also provide heirs with assets that can be withdrawn without additional taxation.

However, Roth conversions increase taxable income, which can affect eligibility for ACA subsidies. This is where the planning trade off becomes important.

The Strategic Tradeoff Early Retirees Face

Early retirees often face a decision between two competing strategies. One approach focuses on structuring income to qualify for ACA subsidizes and reduce healthcare costs. The other focuses on completing Roth conversions to reduce long-term taxes.

Both strategies can be beneficial depending on the circumstances. In some cases, maintaining subsidy eligibility may provide significant savings in healthcare costs. In other situations, accelerating Roth conversions may reduce taxes over the course of retirement.

The key is evaluating how each strategy affects healthcare costs, tax brackets, and future retirement income.

Final Thoughts

Reaching age 60 with $2 million saved for retirement means that the hardest part of the journey has already been completed. However, the decisions made during the next several years can have an outsized impact on long-term financial outcomes.

The years between retirement and Medicare are not simply a transition period. They represent one of the most valuable planning windows available in retirement.

When managed carefully, this window can help reduce healthcare costs, lower lifetime taxes, and create a more efficient retirement strategy. Most importantly, it allows individuals to begin enjoying.

Let's Meet!

.webp)

About the author: Nathan Lee is a CERTIFIED FINANCIAL PLANNER® and Behavioral Financial Advisor at Servet Wealth Management in New York City. He works with individuals and families navigating important financial decisions, including retirement planning, tax strategy, investing, income planning, and wealth management. Through his blog and YouTube channel, Nathan explains complex financial topics in a practical, easy-to-understand way.

I read every email and would love to hear if this blog helped you.

.png)

.png)