.png)

%201.png)

News and Insights

The 7-Figure Retirement Tax Trap Most Pre-Retirees Fall Into

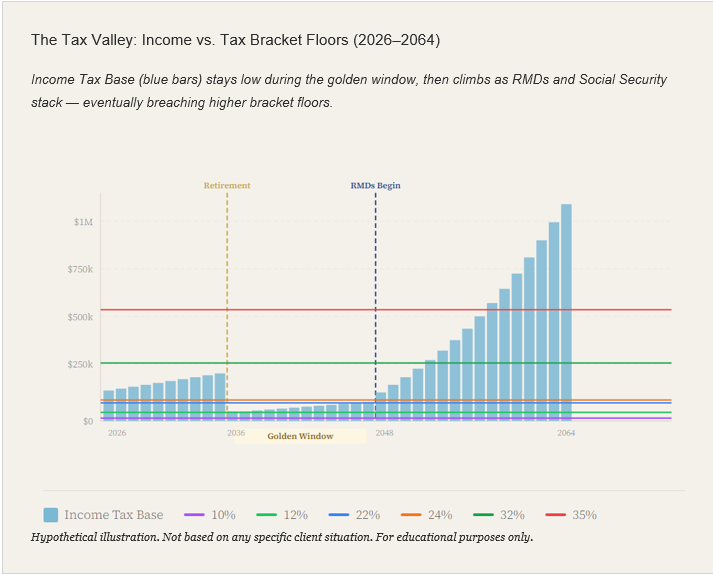

Robert spent 30 years building a $1.8 million IRA and never touched it in retirement. His pension and Social Security meant he didn’t need to. So it continued to grow.

When he turned 73, his first Required Minimum Distribution was just over $140,000 due to the continued growth of his investments.

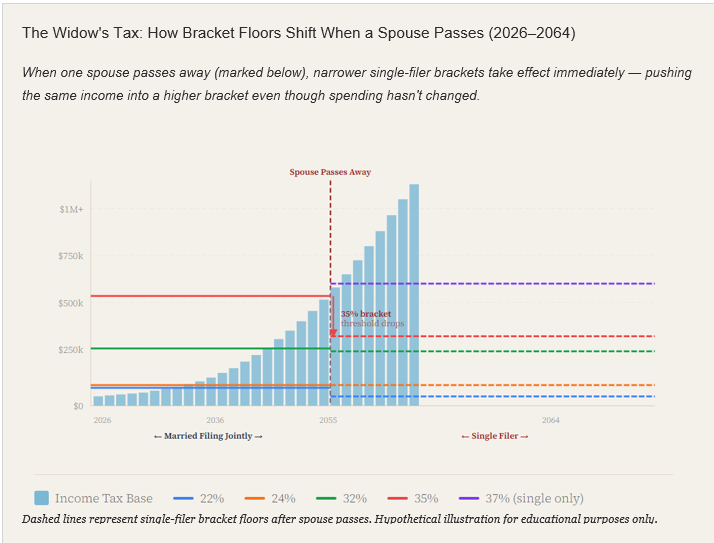

Stacked on top of his pension and Social Security, he found himself pushed into the 32% tax bracket—higher than he’d ever paid during his working years. Not only that, but his wife had passed away a year prior, so he was filing alone.

That 32% bracket was much more narrow, as were his margins.

He wasn’t in trouble, but he was paying significantly more in taxes than he needed to, and it was too late to do anything about it.

Robert’s story is common and something we see often, especially in this bull market we’ve experienced over the past 10–15 years. It’s often the reality for retirees leaning on conventional Roth wisdom that tells them not to touch their IRAs. Traditionally, retirees have been told not to bother with Roth conversions if your tax rate will be lower in retirement.

But there are actually four factors to evaluate before making a Roth conversion decision, not just one. Dealing with them now can help you avoid a Robert situation in the future.

1. Your Current vs. Future Tax Rate, Reconsidered

Your tax rate today versus your expected rate in retirement is absolutely part of the picture. It’s the only factor people don’t tend to skip. The problem is when they stop there.

“I’m in the 22% bracket now, and I’ll probably be in a similar bracket when I retire. So why would I choose to pay more taxes today?”

Yes, writing that check can be painful. But waiting might cost far more.

Say you retire with $1.5 million in a traditional IRA and $500,000 in a taxable account. Social Security helps cover your basic expenses, so you start pulling from the taxable account for income — paying only long-term capital gains rates — and let the money in the IRA keep growing.

On the surface, it feels like a smart move. You’re minimizing taxes today and letting your retirement savings compound.

But there’s a downside. By the time Required Minimum Distributions kick in, that $1.5 million IRA could easily be $3 million. Now every dollar of it is pre-tax. You’ve spent down your taxable account, so now you’re left with a massive pile of ordinary income the IRS is about to force you to take whether you need it or not.

Add those withdrawals on top of the pension, Social Security, and other income, and suddenly you’re in a significantly higher tax bracket.

This window is most impactful for those with large IRA balances who won’t need to draw from them in early retirement. If you’re drawing from your IRA right away, the RMDs may be smaller, so it matters less. But for those with a large, untouched IRA, the golden window is among the most critical planning opportunities you have.

2. The Widow’s Tax

Most Roth conversion conversations focus entirely on the account holder: their bracket, their RMDs, and their retirement income. Too often, the big picture of what retirement looks like for a married couple goes ignored.

For married couples, the tax math works in your favor while you’re both alive. When filing jointly, you benefit from wider tax brackets and more manageable Medicare premiums. But at some point—statistically likely with a retirement that lasts two or three decades—one spouse will pass away.

When that happens, the surviving spouse shifts to a single taxpayer. That alone can push them into higher tax brackets.

Income that had you both in a 24% bracket can turn into a 35% bracket as a single filer without any change to your income.

Then there’s the matter of IRMAA. These are surcharges on Medicare Part B and Part D premiums that phase in at lower income thresholds for single filers than for married couples. As a result, the surviving spouse could be paying more in income taxes and higher Medicare premiums.

Roth conversions during the golden window address this directly. By converting more in those early lower-income retirement years, you reduce the IRA balance and future RMDs, which keeps income lower for the surviving spouse. Done well, this can mean the difference between staying in a mid-20% range versus being pushed into the mid-30% range for the rest of their life.

3. Your Children’s Tax Rate

You spend decades deferring taxes to preserve wealth, unknowingly leaving it to your kids to pay those taxes at a higher rate than you would have. This is not a hypothetical—it happens to a lot of high-income families.

Under the current rules (specifically the SECURE 2.0 Act), most non-spousal beneficiaries, including your children, must fully withdraw an inherited IRA within 10 years of the original owner’s passing. No more “stretching” distributions out over a lifetime.

Accounts are often inherited by people in their 40s or 50s when they’re likely earning peak salaries, receiving bonuses, and collecting equity compensation. Layer inherited IRA withdrawals on top of that income, and the tax consequences can be extreme.

When you convert to Roth, your children still must distribute the account within 10 years, but those distributions are generally tax-free. More of what you build ends up in the hands of your heirs rather than Uncle Sam's.

Now, this doesn’t apply to everything. If your estate will be divided among several children, or your heirs are in lower income brackets, there’s less urgency. It’s really a consideration for families with high-earning heirs.

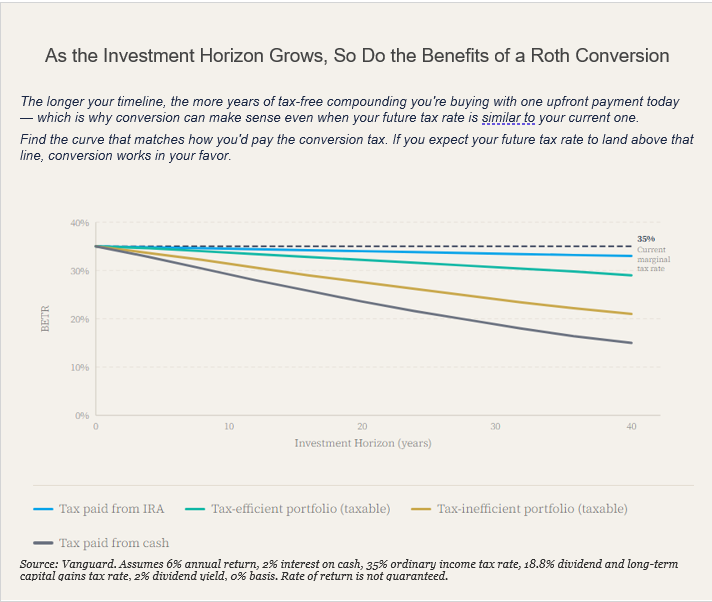

4. The BETR Framework

After walking through the first three factors, I often hear something like, “But if I expect to be in roughly the same tax bracket in retirement as I am now, does any of this even apply to me?”

Yes—when you consider the Break–Even Tax Rate (BETR) framework, developed through Vanguard research.

Traditional analysis compares your tax rate now to your future retirement tax rate. That’s it. It ignores ongoing taxation on your taxable brokerage account. Dividends, interest, and capital gains distributions are all generating taxable income every year, whether you reinvest or not.

Say you convert $100,000 from a traditional IRA and pay the tax using money from your taxable brokerage account. The $100,000 now grows inside the Roth without taxes on dividends, capital gains, or distributions.

The comparison is a one-time payment now against decades of ongoing annual taxation, not just today’s rate against tomorrow’s. Conversions can come out ahead even with comparable tax brackets.

So, Should You Make Roth Conversions?

Nobody knows exactly what their tax rate will be 10 or 20 years from now. Tax law, income, and life changes. That uncertainty is precisely why a single-variable approach can’t anchor your decision alone.

The four factors won’t tell you definitively to convert, but they do point you in the direction of which questions to ask:

- Is there a golden window available to you, and are your IRA balances large enough that RMDs will become a problem down the road?

- If you're married, what happens to your spouse's tax situation when you're gone — would conversions now protect them later?

- Are your heirs in their peak earning years, and would a Roth inheritance keep significantly more in the family?

- Do you have a taxable brokerage generating annual taxable income, where a one-time conversion tax might beat paying that drag indefinitely?

The problem most people, like Robert, make is in unexamined assumptions, such as defaulting to tax rate comparisons, which leave room for gaps that can cost tens of thousands of dollars. You likely have time to do differently.

Content in this material is for general information only and is not intended to provide specific advice or recommendations for any individual.

Let's Meet!

About the author: Nathan Lee is a CERTIFIED FINANCIAL PLANNER® and Behavioral Financial Advisor at Servet Wealth Management in New York City. He works with individuals and families navigating important financial decisions, including retirement planning, tax strategy, investing, income planning, and wealth management. Through his blog and YouTube channel, Nathan explains complex financial topics in a practical, easy-to-understand way.

I read every email and would love to hear if this blog helped you.

.png)

.png)