.png)

%201.png)

News and Insights

You Can Retire Before 60 — But Only If You Do These Things in Your 50s

I’ve worked with people who had several million dollars saved yet still couldn’t pull the trigger on retirement. I’ve also worked with others who retired confidently and comfortably at 58 with far less.

In every case, the deciding factor was preparation, not portfolio size, timing, or a stroke of good fortune. There was no perfect allocation or magic number. Knowing their true expenses, testing their plan while still working, and solving early-retirement problems before they arrived made the difference.

You don’t need to check every single box here to retire early, but each one makes the next step easier.

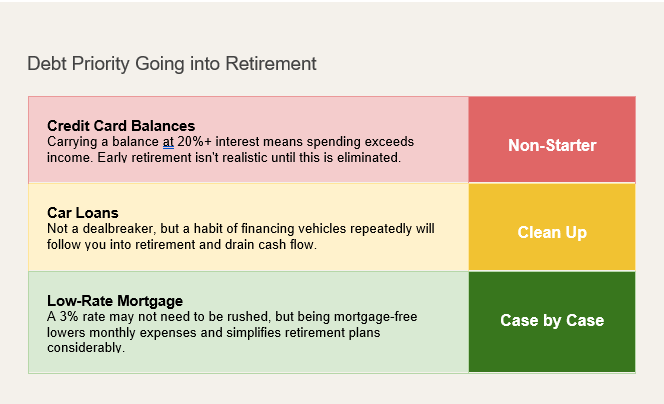

Resolve Your Debt Situation

Debt doesn’t automatically disqualify you from an early retirement, but it does make things more difficult by raising your required monthly income, limiting your flexibility, and adding an extra layer of pressure to your plan.

A 3% mortgage is a different conversation than a 20% credit card balance. The former might make sense to carry forward if your investment growth outpaces that rate. But the latter means you may not be living within your means right now, which is a problem retirement can’t fix.

That said, financial planning is sometimes about doing the second-best thing and being able to sleep at night rather than the “optimal” thing that creates more stress. For a lot of people, being completely debt-free, even when you can technically carry the mortgage, is what gives them the confidence to finally retire.

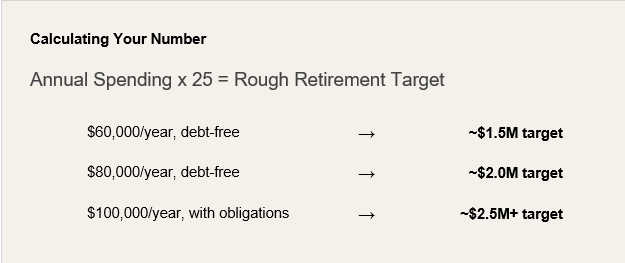

Know Your Lifestyle Number

Headlines will tell you to have $1 million or $2 million to retire. Ignore them. Those figures are just averages that don’t account for where you are or what you want your retirement to look like.

A lifestyle that costs $60,000 a year but is debt-free is one retirement. But if your lifestyle costs $100,000 a year and you’re still carrying debt obligations, that’s a different plan, but still workable.

Get this right and everything downstream becomes clearer: how much you need to save, how your portfolio should be allocated, and when you can realistically step away from work.

How to Test Your Retirement Budget Before You Retire

One of the most practical things you can do in your 50s is start living on your retirement budget now, while you’re still earning. If you think you can live comfortably on $5,000 a month, try it.

If it doesn’t work, you’ve found out early enough to fix it. If it does work, you’ve just proven to yourself that early retirement is realistic. Any extra money you don’t spend goes towards building cash reserves or paying down debt faster.

Build a Cash Reserve That Doesn’t Budge

The worst sequence in early retirement is retiring into a downturn and being forced to sell investments at a loss to cover living expenses. Planners call this sequence of returns risk, and a cash reserve is a direct defense against it.

Before retiring early, I’d want to see at least one year of living expenses sitting in cash or a short-term bond equivalent. If your retirement costs $60,000 a year, that means $60,000 in an accessible, safe account—not invested, illiquid, or at risk. When markets pull back, you can draw on that cash instead of selling and give your portfolio time to recover without needing to participate in the loss.

This reserve isn’t meant to earn returns. It’s there to buy peace of mind and time when you need it. That said, a money market account with a reasonable yield is a sensible place to park it for some return with minimal risk.

Structure Your Income in Layers

A well-built early retirement income plan isn’t one thing; it’s three. Your cash reserve is an ongoing liquidity buffer to maintain throughout retirement. Your investment portfolio handles

long-term growth. The middle layer — the bond ladder — bridges the years in between, offering a better yield than cash without as much market volatility.

A bond ladder means purchasing Treasury bonds or high-quality corporate bonds that mature in consecutive years. One set matures in year two, another set in year three, and so on out to year five or six. Each maturity covers that year’s living expenses, so you don’t have to rely on the market to be up every year. You’re also not stuck sitting on pure cash that earns next to nothing for five years.

Cash is the right tool for near-term liquidity, as it’s fully accessible and carries little risk. But holding five years of expenses in cash means accepting a return that often trails inflation. Bonds in the 2-5 year range typically offer meaningfully higher yields than a savings account while still giving you near-certainty that the money will be there when you need it.

This structure works best for people with a substantial taxable account outside of their 401(k) or IRA, as you need accessible funds to purchase the bonds. But even if most of your savings are in tax-advantaged accounts, the ladder is still worth building inside those accounts. The same logic applies — you know exactly where each year’s withdrawals are coming from, and you’re reducing the volatility that comes from needing to sell investments on the market’s schedule, not yours.

One note on inflation: bonds are not a true inflation hedge. Fixed-rate bonds lose value when inflation runs high, because the coupon payment is locked in. What the ladder offers is a better return than cash over a 2–5 year window, with near-certainty of outcome.

If inflation is a primary concern of yours, TIPS (Treasury Inflation-Protected Securities) are instruments specifically designed to adjust with inflation.

High-quality corporate bonds often yield slightly more than Treasuries while still offering strong confidence that the principal and interest will be paid at maturity. Ultimately, the goal of the ladder is to know where years two through five are coming from, so the portfolio can do its job without being interrupted.

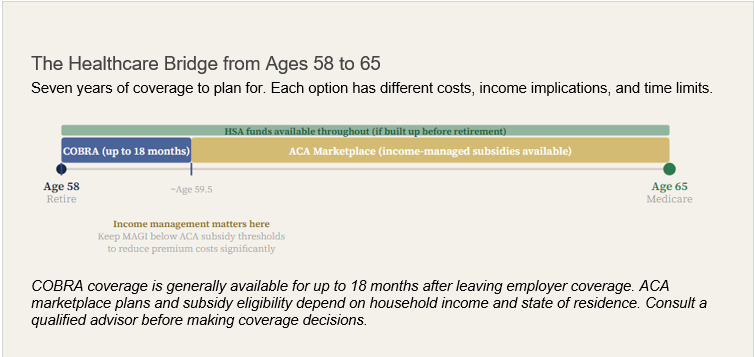

Solve the Healthcare Equation

If you retire at 58, you have seven years before you’re eligible to enroll in Medicare. The price tag of health insurance can catch people off guard when they’re stuck in the space between employer-sponsored coverage and Medicare.

The cost of unplanned healthcare goes beyond the premium, too. A single significant medical event without adequate coverage can derail a solid retirement plan, so filling this gap before you retire is non-negotiable.

During the years you're on ACA marketplace coverage, your premium subsidies are tied to your taxable income. Managing income carefully during this period and keeping it below certain thresholds can reduce what you pay for coverage. This intersects directly with the Roth

conversion conversation, since conversions add to taxable income for the year. The timing of both decisions needs to be coordinated intentionally.

The Golden Window for Tax Planning

The golden window is the period between when you stop working and when Required Minimum Distributions (RMDs) begin. For early retirees, it can last a decade or more.

During this window, your taxable income is often at its lowest point. You're no longer earning a salary, Social Security hasn't started yet, and RMDs are years away. That creates an opportunity to reposition assets to reduce future tax liabilities.

If you're managing income to qualify for ACA subsidies, Roth conversions add to your taxable income for the year. Push too far, and you lose the subsidy. This is where utilizing COBRA coverage in the first 18 months of retirement can sometimes create useful flexibility, as it gives you room to do conversions before you need to carefully manage income for ACA purposes.

I've worked with clients who retired at 58 and used this window to convert substantial amounts into Roth IRAs at very low rates. Over time, that translated into six figures in tax savings.

Simplify Before You Retire, Not After

Retirement shouldn’t require active management to function. If you spend the first years of retirement logging into five different accounts, manually tracking withdrawals, and trying to remember which custodian holds what, you’re effectively working a part-time job.

The "multiple income streams" concept gets a lot of attention, but for most retirees, a properly allocated portfolio is all the income stream they need. If you happen to already have rental income or a small business, that's great!

That said, building complexity into your finances on the eve of retirement isn’t ideal.

Handle Predictable Expenses Beforehand

Retirement won't be free of surprises. There will always be a new roof, a car replacement, or an unexpected expense you can’t have known to budget for. What you can control is whether you're also carrying predictable, foreseeable obligations when you retire.

College costs, weddings, co-signed loans, and ongoing support for adult children are all known expenses. If they're still there when you retire, they not only strain your budget but risk creating resentment when every dollar going to an obligation is a dollar not going toward the retirement you planned.

Resolve the ones you can so you have the flexibility to absorb the ones you can’t.

“I Think I Can” Versus “I Know I Can”

Retiring before 60 comes down to whether your finances have been built to support a specific, tested, realistic life — and whether the problems that tend to surface in early retirement have been dealt with ahead of time.

The people who retire confidently at 58 did the preparation: they resolved their debt, tested their budget, built a cash reserve, solved healthcare, structured income, simplified their accounts, and cleared the predictable expenses before making the jump.

Most of these aren't complex strategies. The challenge is doing them consistently, far enough in advance, while you're still in the best position to act.

Content in this material is for general information only and is not intended to provide specific advice or recommendations for any individual.

Let's Meet!

About the author: Nathan Lee is a CERTIFIED FINANCIAL PLANNER® and Behavioral Financial Advisor at Servet Wealth Management in New York City. He works with individuals and families navigating important financial decisions, including retirement planning, tax strategy, investing, income planning, and wealth management. Through his blog and YouTube channel, Nathan explains complex financial topics in a practical, easy-to-understand way.

I read every email and would love to hear if this blog helped you.

.png)

.png)